|

The twentieth annual conference should be recorded in the annals of the International Corporate Governance Network as being a successful conference. From small beginnings twenty years ago, when 49 hardy souls met, the ICGN annual conference has grown ten-fold. Nearly 500 delegates assembled (from close to 50 countries) at the Guildhall in London to listen, share and, importantly, to exchange experiences.

Was the conference worthwhile? If the quality of the insight, discussions and relationships are any indication, the answer must be 'yes'! Consequently, the 21st edition is already marked my diary.

1 Comment

Martin Wolf CBE, Associate Editor and Chief Economics Commentator at the Financial Times, delivered a rousing keynote talk to wrap up the final day of the ICGN annual conference. After observing that the limited liability, joint-owned corporation had been the cause and consequence of almost all economic activity over the last two hundred years, Wolf posed and commented on four questions. He qualified his comments by saying that he expected they might raise some profound questions. Indeed, some of Wolf's comments were controversial—the evidence being the questions asked by some members of the audience after he finished speaking. What is a limited liability corporation? They are a semi-permanent entity designed to outlast small-medium enterprises (because founders retire—the corner store conundrum) and markets, and they are a construct for the consolidation of relational and implicit contracts. Their genius is the importation of older hierarchical forms (to get things done) into the market system. With scale comes efficiency, endurance and effectiveness (but not always!). What is their purpose? The apparent purpose of the LLC is to generate economic value. However, this is insufficient. Wolf asserted that LLCs should also pursue a wider remit, by seeking to 'add value' in social terms (through the provision of payments for services rendered—wages and salaries—for example). What is their operational goal? The oft-quoted goal, of maximising shareholder returns, is far too simplistic, according to Wolf. It is selfish and can only lead to failure elsewhere in society. Rather, the operational goal of LLCs needs to include ethical constraints to protect all participants and in so doing ensure the good of society (at no point did Wolf pursue or even imply any form of Marxist agenda). Who should control them? Economically, shareholders bear residual risks following corporate activity and, therefore, shareholders should possess control rights. Wolf challenged this commonly-held view as folly because shareholders are unable to exert full control over the affairs of the corporation. Managers may manipulate the affairs of the company, sometimes to the detriment of shareholders and other stakeholders. Short-term incentives, implemented to motivate managers towards the maximisation of shareholder returns, rarely position the company for longer-term success. Wolf concluded by saying that LLCs are a wonderful construct. However, he went on to say that the two associated doctrines (of shareholder control and value maximisation) are unhelpful because they are too short-sighted. He told the shareholders in the room that "it is in your interest not to control the corporation completely". Other parties—large bondholders, for example—also bear residual risks. Why would they not have decision rights? Wolf's comments were demonstrably controversial (amongst some of the audience at least). However, the poor reputation of big business amongst the general populace suggest Wolf's comments might be closer to the 'truth' than what many in the audience might care to admit. Wolf closed with this demanding challenge: A better approach might be "to let a hundred flowers bloom", so that the best [control] model might rise up and be applied for a given situation—the beneficiary being society at large.

The second panel discussion of the third (and last) day of the ICGN conference looked to the future. The topic brought together many of the discrete threads from earlier conversations. Here are some of the takeaways:

These takeaways demonstrate that boards are starting to thinking about future business performance. However, there is much work to do, both by boards to determine an appropriate division of labour between the board and management, and by shareholders to express their wishes more clearly than perhaps now is the case.

Day 3 of the ICGN annual conference opened with a lively panel discussion on the subject of sustainability reform. From the title of the session, I thought the conversation would explore ways and means of reforming the capital market in the fight against short-termismthe goal being longer-term corporate value and sustainable economic growth. However, the conversation was actually about the ESG (environmental, sustainability, governance) agenda. The starting point for the conversation what that shareholders need to change their mindset, away from short-termism and quarterly results, towards the long term prospects of the company, for the good of the economy and the well-being of society. Regulation was identified as being important (and probably necessary) if the desired behaviour change was to occur. However, there was little appetite for a new regulatory regime to expedite change. Rather, the panel thought professionalism was a far better vehicle—on the basis that professionalism well implemented should reduce the need for prescriptive regulation. Notwithstanding this, a reasonably significant shift in behaviour is likely to be required (amongst shareholders and the board) if companies are to respond positively to the sustainability expectations of customers, suppliers and the general public. Institutional investors probably need to step up and become part of the conversation, both to move their focus beyond the ninety day cycle and to pressure management into embracing sustainable business practices. The panel was asked how this move towards professionalism could be effected. One popular and readily implementable option was to use the AGM as a forum to raise questions. If institutional investors were to speak publicly (at the AGM) on matters of climate change, sustainable business practices and responsible business practice (for example), and do so in a firm but fair manner, then others (including the press and smaller investors) would notice. In so doing, astute directors and managers would respond by adjusting various priorities. Much of the conversation was focussed on structural responses to identified problems. However, the ante was raised somewhat towards the end of the session, when an audience question shifted the conversation. Panel members were asked for their thoughts on how to drive desirable (sustainability) behaviours in the boardroom. After some um-ing and ah-ing, the following three items were proposed:

This seemingly 'thin' response exposed another problem: that investors may not think about what goes on in the boardroom as much as some might think or hope. This probably needs to change. Standing back a little, the session explored a different question from the one I expected to be tackled. However, the discussion was very helpful because it demonstrated that change is possible if the right sort of pressure and catalyst is brought to bear. The power of the AGM as a suitable forum to raise questions and exert pressure on the board and management of companies should not be underestimated for example.

Robert AG (Bob) Monks is a experienced shareholder activist and pioneer in corporate governance. The tall octogenarian has spent a lifetime influencing boards and board performance, especially in corporate America. Monks was invited to deliver the keynote address the ICGN conference. Monks, a gifted orator, spoke from the heart, and he had the gathered delegates enthralled as he did so. Reviving memories of the wartime leader Winston Churchill, Monks reminded delegates that, while they had come far, they were not at the end (ie. 'arrived') nor were they at the beginning of the end. They were, he said, "at the end of the beginning". He went on to suggest:

Monks continued by offering several recommendations to the audience (comprised largely of institutional investor representatives but also other participants in the corporate governance community including academics and advisors). He said that shareholders need to be genuinely engaged (by specifying what they want from their investment); that integrated reporting is crucial (to provide clarity around actual business performance); and, that all publicly-listed companies need to have real (identifiable) owners (to satisfy the engagement challenge. Monks received a standing ovation from some of the delegates, such was the power of his oratory and the high esteem in which he is held. One surprise: neither value creation or strategy was mentioned. I wonder what Monks thinks about these activities and the board's role therein. Rather than guess, I'm going to ask him. Congratulations to the conference organisers for securing Bob Monks' contribution to the debate.

For many of us, the boardroom is an opaque structure, whereby those on the outside can only but guess what might (or might not) happen on the inside. And that's the way many directors like it: strong norms of privacy and claims of confidentiality are held up as defences against such things as professionalism and accountability. While many boards try to do their job well, some directors are victims of hubris, arrogance, laziness and, in some more extreme cases, a perception of being above or beyond the law (the slippery slope that often leads to fraudulent activity). It's little wonder that the level of distrust (of directors) is at an all-time high. The second plenary of the second day of the ICGN conference tackled the topic of what does (well, should) happen in boardrooms. The panel prized open the corner of the blackbox.Here's some of the takeouts from the discussion:

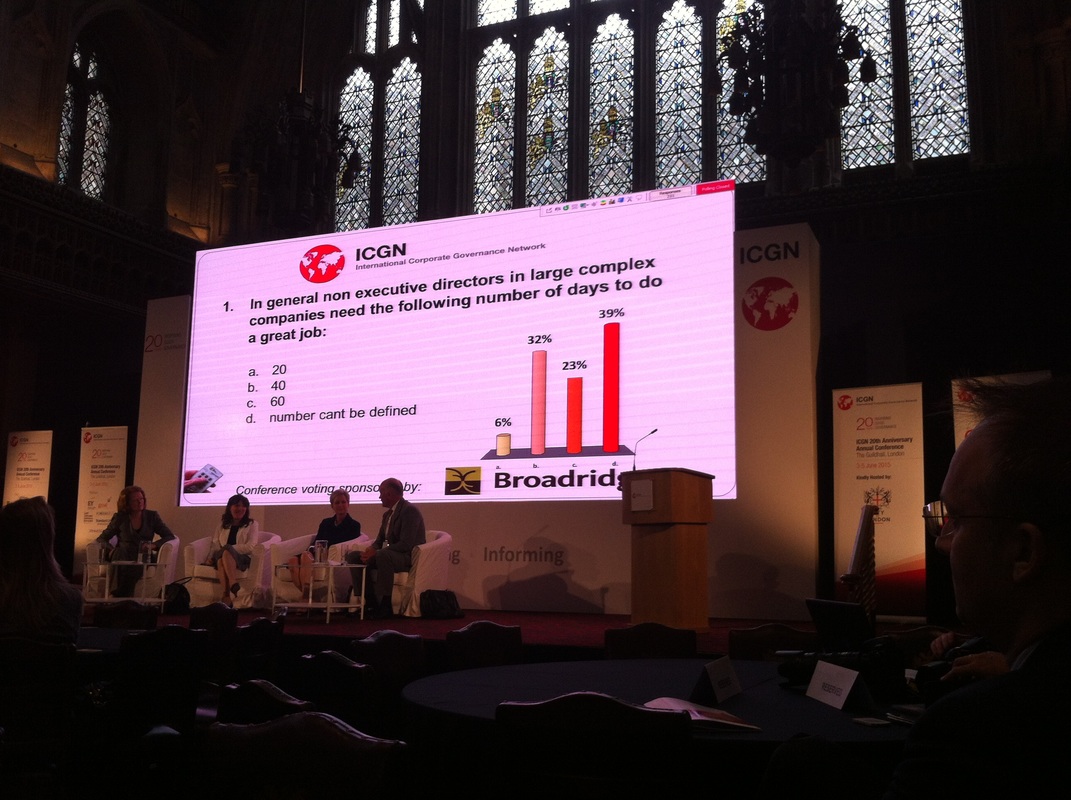

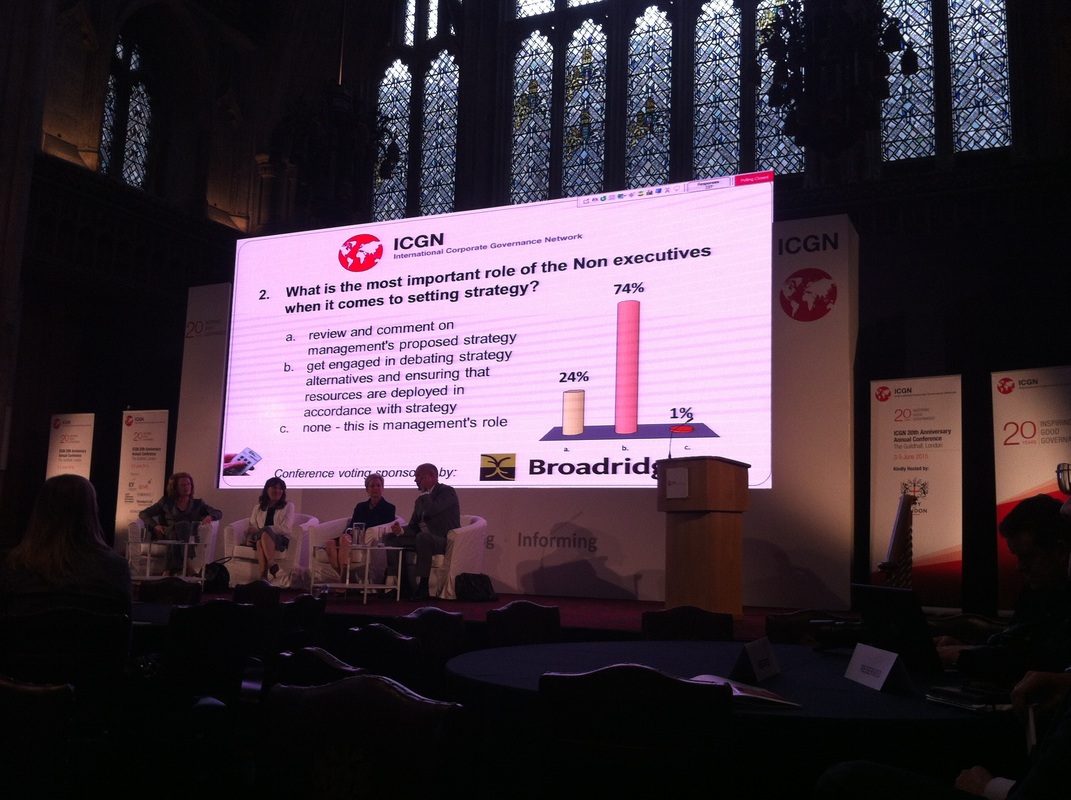

My experience, both as a serving director and as a silent observer is that the characteristics listed above are probably necessary to board effectiveness. However, they are by no means sufficient nor do they necessarily guarantee business performance outcomes will be achieved. I was surprised that little attention was paid by the panel to time splits (compliance / monitoring / forming future strategy) or to the importance of strategy as a board agenda item. This would have been useful guidance for serving directors. However, it is probably a touchy subject. Most directors 'know' how much time they perhaps should spend on strategy (and they'll 25–40 per cent if asked), whereas most boards actually spend far less time on this activity (typically five per cent). Perhaps this discrepancy is a source of embarrassment to directors and, therefore, it does not get discussed. Notwithstanding this, this discussion as probably the most useful of the conference to date—because it was about boards and what boards [should] do (ie. corporate governance).

The topic of the first plenary of Day #2 of the ICGN conference was whether the time had arrived for an holistic review of the financial market regulatory framework. This question was timely because most of the standard 'hard law' responses (to failure) have done little more than to increase the compliance burden that companies needed to deal with. The panel was quick to acknowledge this. It suggested that an holistic review was needed, and warned that genuine change would only occur if several desirable behaviours (I'd call them 'social commitments') were embraced alongside the hard law responses. The following social commitments were discussed:

This discussion was as interesting as it was disappointing. To the average man in the street, an holistic framework incorporating hard rules and social commitments makes good sense. The disappointment was that the discussion was even needed. Clearly, some boards remain reluctant to make (let alone embrace) the social commitments. Given this, it is little wonder that 'big business' has such a poor reputation amongst the general populace.

Sophie L'Helias, Senior Fellow, Governance at Governance Board chaired a very interesting panel discussion. The panel was asked to discuss whether corporate governance had progressed or regressed over the last twenty years (since ICGN was formed). The opening observation was that much had changed, yet much remained the same:

This first panel session of the conference provided an interesting opening play, upon which later discussants could build (or otherwise!). The main takeaway for me was that shareholders and boards need to 'grow up'. Looking over the fence at each other (and, in some cases, simply ignoring each other) is not a healthy context for either productive ownership or effective control. Boards were created to bridge between owners and managers, yet many boards seem to be far more interested in pursuing their own interests and priorities (than acting in the best interests of the company or the shareholders). While we appear to have come far, we still have much to learn.

Alderman Alan Yarrow, Right Honourable The Lord Mayor, City of London provided the official welcome address straight after the ICGN AGM. Yarrow's speech was short and sharp, and it was delivered with great enthusiasm. Looking back over the last twenty years, Yarrow observed that while much appeared to have changed in the corporate governance world, much more had not. He went on to suggest that, with the benefit of hindsight, many seemingly good decisions made in good faith actually had unintended consequences. For example, many of the reforms introduced in the 2008–2010 period in response to the GFC did not deliver the expected benefits. Rather than tidy up company operations and reporting regimes, they have decreased liquidity, increased the rate and extent of change; and, increased the volatility of markets. An enlightening observation. Baroness Neville-Rolfe spoke after The Lord Mayor. Neville-Rolfe is a recently re-elected Conservative MP in the British House of Commons. Her speaking engagement at ICGN was her first 'outing' (to use her word) since the election results were confirmed. She claimed to be in listening mode, to find out what was going on and to learn about emerging trends in the world of commerce. More specifically, the Baroness invited the corporate community to express its view and to make recommendations. However, the Baroness was not without opinions herself. Having issued the invitation, she went on to suggest that the following attributes are important for 'good governance'.

Together these two speeches were as wonderful as they were brief. They set the scene for the conference very well. I could have listened to these two speakers for longer, but sadly their time was at a premium.

If you are anything like me, Annual General Meetings do not normally feature as compelling events in your calendar. AGMs are often boring sequences of compliance-oriented voting, with little if any inspirational or aspirational commentary. Most of the time, I give AGMs a wide berth. However, as a new ICGN member, I decided to attend the AGM to hear the discussion, and I'm pleased for the experience. The chairman, Erik Breen ran a good meeting and every resolution was carried. On first contact, the ICGN feels like 'just another' corporate governance body. However, having listened through the AGM, I was pleasantly surprised to find:

While the ICGN was birthed out of the investor community (53% of the membership today is from this community) to support multi-national investment activity, a trend away from investor dominance is readily apparent. The organisation has a clearly stated goal of reducing the dominance of the investor membership increasing corporate and individual membership. One minor disappointment was that there was little mention of individual directors during the AGM. Rather, the focus was on the investor/advisor community—indicative language being 'investors', 'advisors' and 'the company'. This led me to wonder about the ICGN's commitment to championing the task of directing and to holding directors accountable for doing their job properly. The outgoing deputy chairman and finance committee chairman, Frank Curtiss, was recognised for his significant contribution of many years. Anne Simpson received the ICGN Award having been nominated by Sir Adrian Cadbury and Nell Minnow amongst others. This very popular decision was well received by the assembled membership.

|

SearchMusingsThoughts on corporate governance, strategy and boardcraft; our place in the world; and other topics that catch my attention.

Categories

All

Archives

February 2024

|

|

Dr. Peter Crow, CMInstD

|

© Copyright 2001-2024 | Terms of use & privacy

|