The twentieth annual conference should be recorded in the annals of the International Corporate Governance Network as being a successful conference. From small beginnings twenty years ago, when 49 hardy souls met, the ICGN annual conference has grown ten-fold. Nearly 500 delegates assembled (from close to 50 countries) at the Guildhall in London to listen, share and, importantly, to exchange experiences.

- While all of the speakers and panel members were of a high calibre, Alderman Alan Yarrow, Bob Monks and Martin Wolf stood out. Drawing on their vast experience, each of these gentlemen offered perspectives and insight that many of the younger delegates are unlikely to have considered previously.

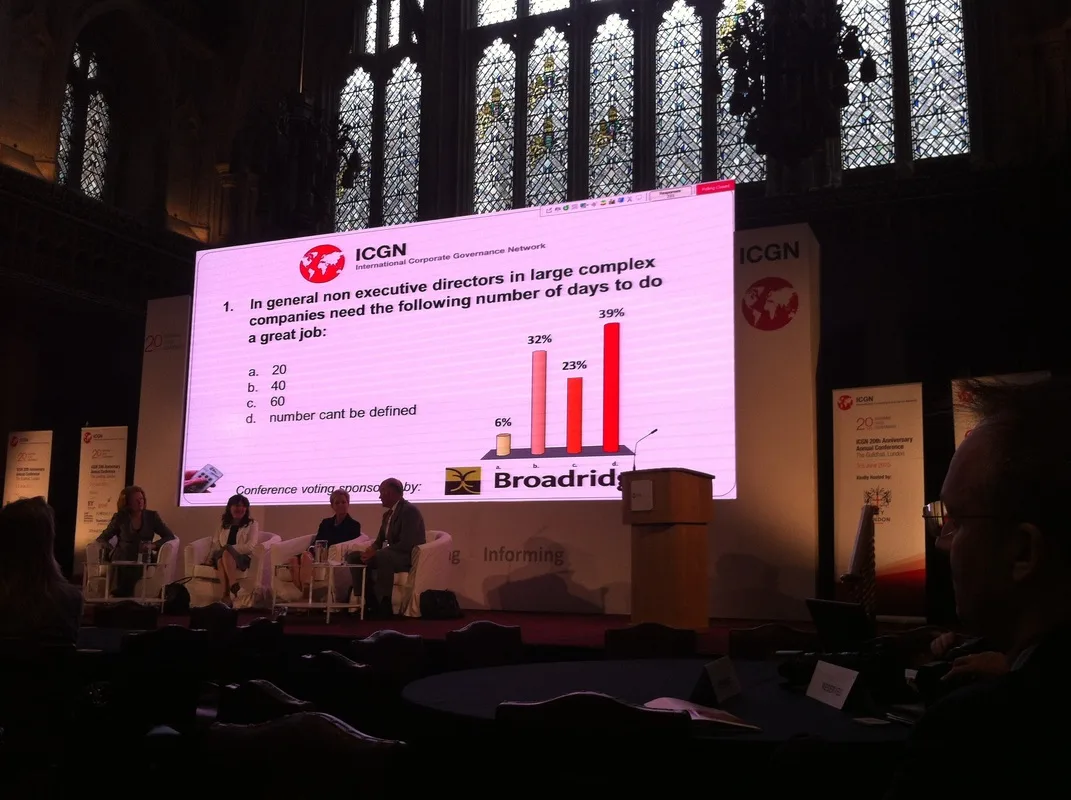

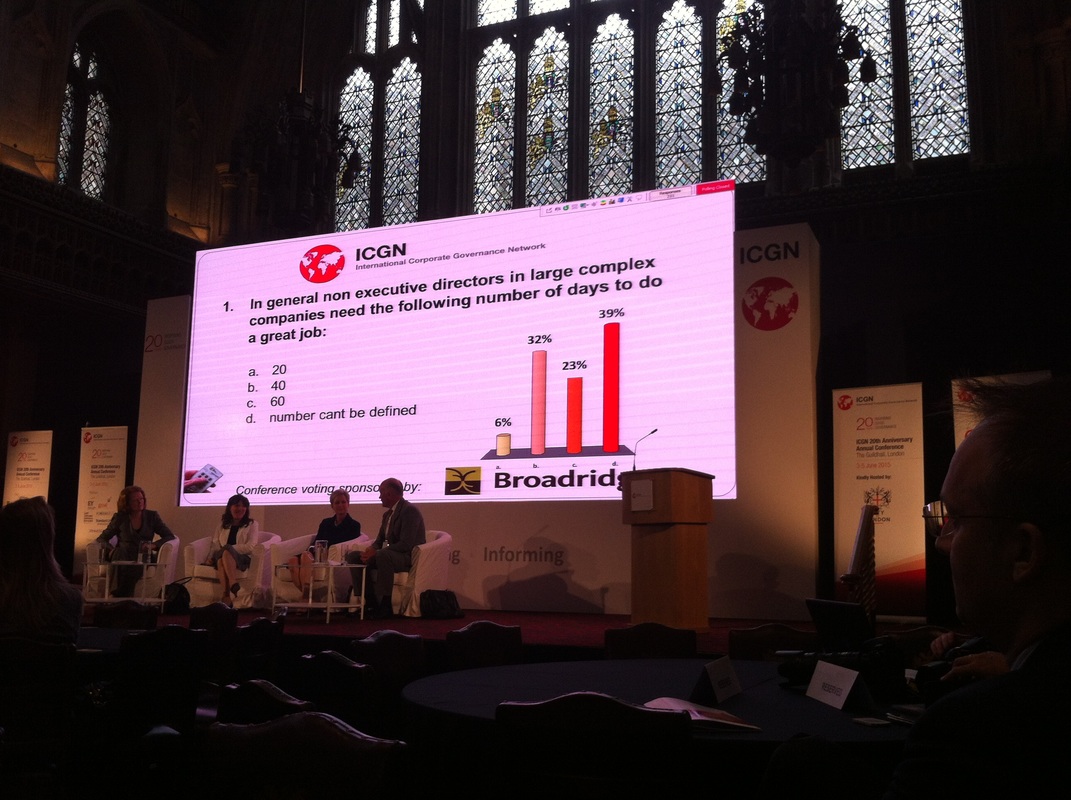

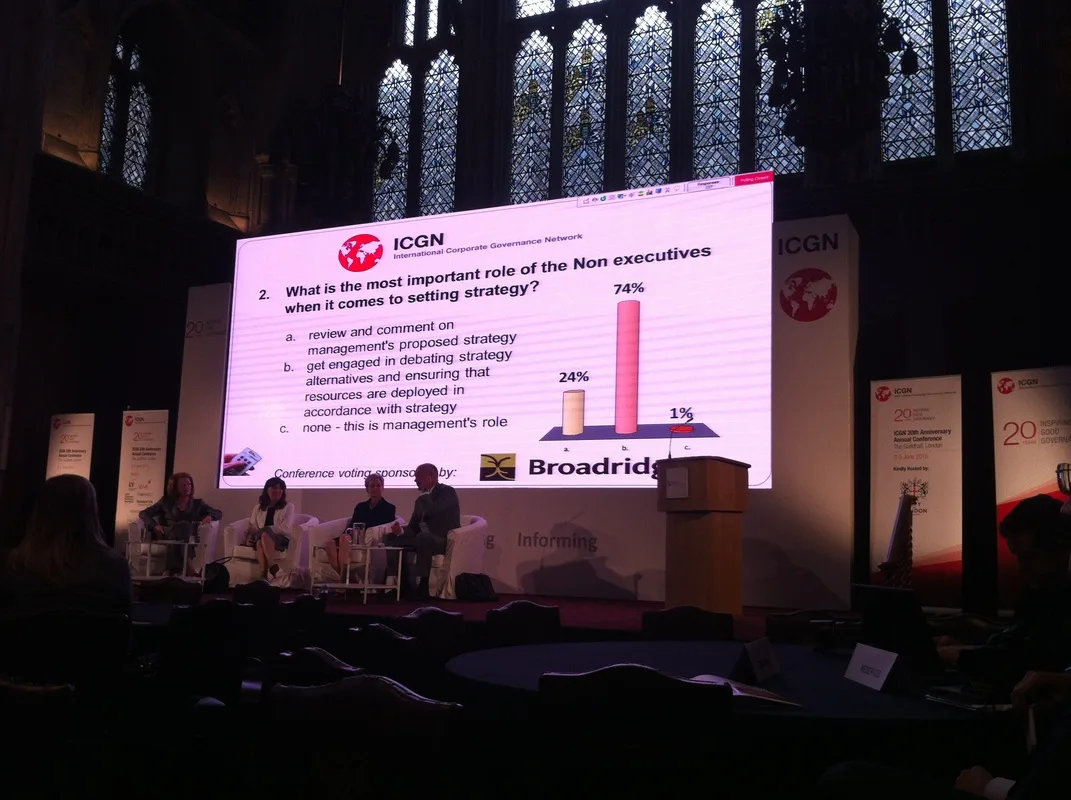

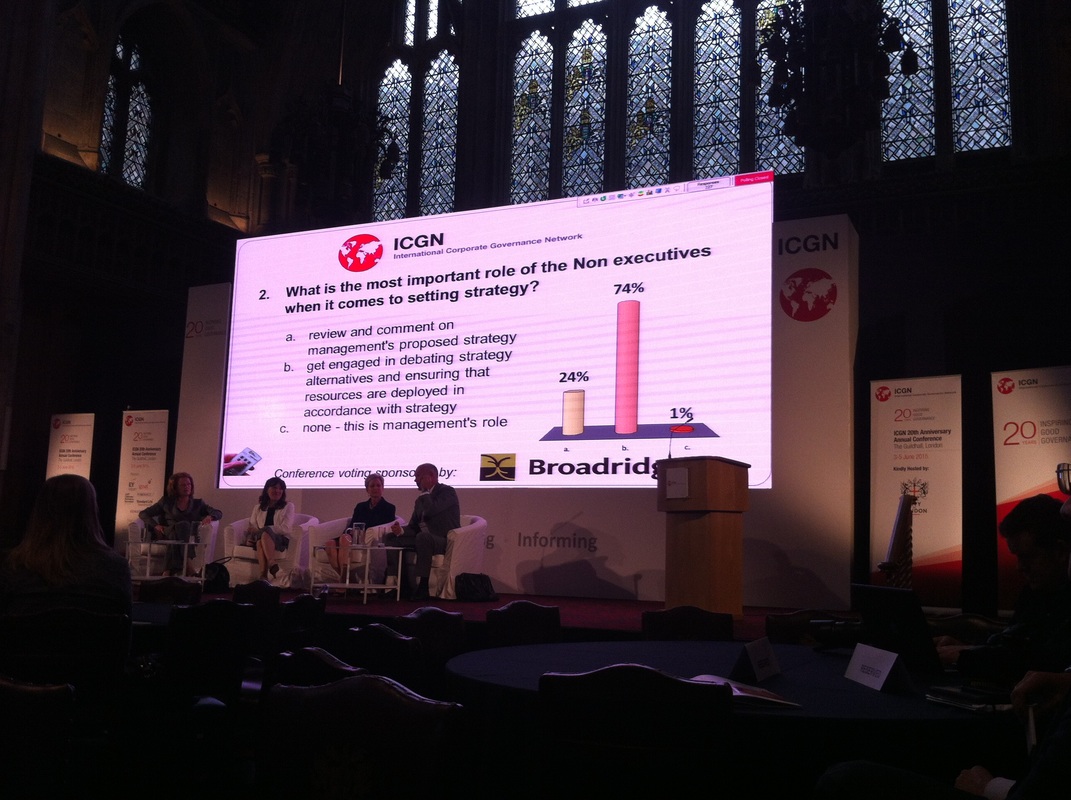

- The unspoken conception of corporate governance that seems to pervade the conference (as something that helps investors get what they want) surprised me. My understanding of corporate governance concerns the way boards of directors work, both in oversight of management and in pursuit of desired outcomes. This surprise may simply have been one of perspective—many of the delegates and speakers are members of the investor community, whereas much of my experience is from within the boardroom.

- Another surprise was the disparity between who I thought might attend this conference and who actually did. The delegate list was dominated by institutional investor and industry body representatives, advisors and lawyers with some academics to boot. However, there were precious few serving company directors in attendance. Serving directors are a (the?) crucial cog in the corporate governance ecosystem. Perhaps the organisers might wish to consider how to redress this imbalance at future conferences.

- The matters of trust (between directors on a board, and between shareholders and the board) and reputation were visible throughout the conference, and rightly so. That big business suffers a troublesome reputation amongst the general populace was noted publicly and it was discussed further over the tea-cups—although whether any remedial actions are forthcoming remains to be seen.

- The conference was well-organised and well-run, and the venue was, simply, stunning.

- The organisation (which prefers to think of itself as a network actually, it's less hierarchical) appears to be in good health. Kerrie Waring is a capable leader. She and her team clearly have the best interests of the organisation, and its goal of lifting the standard of corporate governance, at heart.

- More personally, I met some amazing people (including some that, to this point, had been but names or acronyms on social media exchanges) and had some very helpful discussions. My intention was to watch and to take it in. That others saw it fit to invite me to join their discussions was humbling indeed.

Was the conference worthwhile? If the quality of the insight, discussions and relationships are any indication, the answer must be 'yes'! Consequently, the 21st edition is already marked my diary.