The second panel discussion of the third (and last) day of the ICGN conference looked to the future. The topic brought together many of the discrete threads from earlier conversations. Here are some of the takeaways:

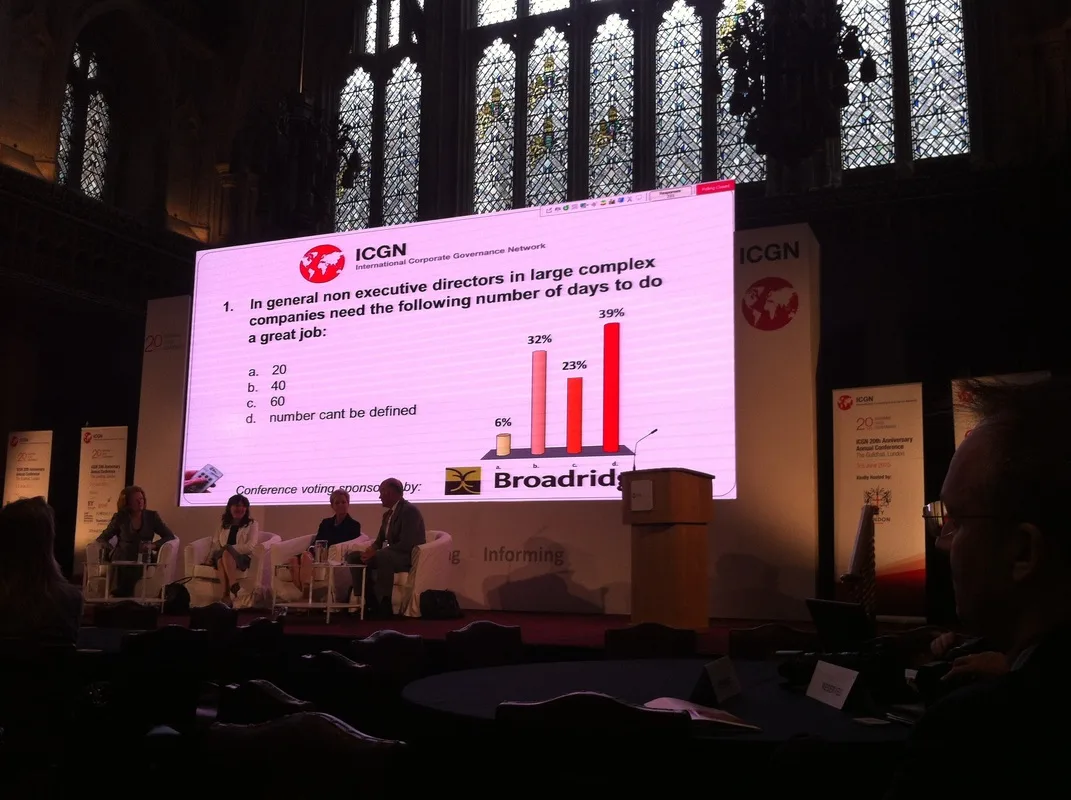

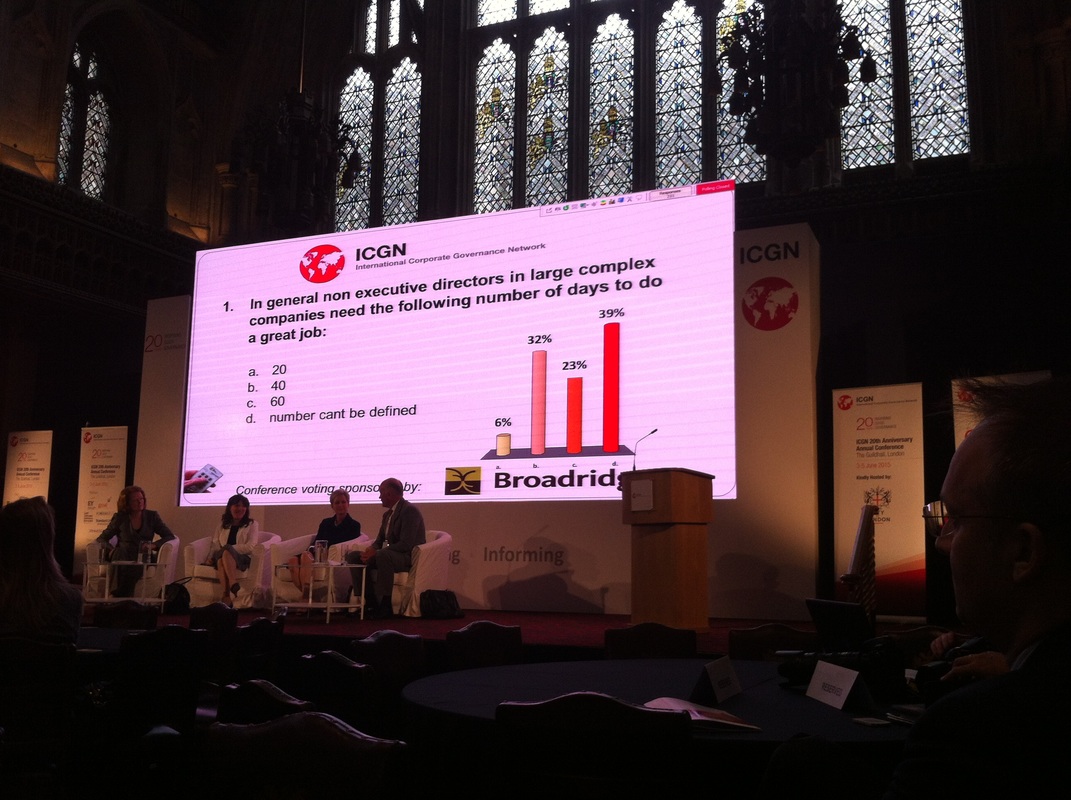

- Directors' expectations of themselves are climbing. About 30 hours per board per month is now considered to be average. The trend towards much higher levels of involvement and accountability is well established.

- There appears to be a significant difference between the amount of time that the directors spend working on the boards of publicly-listed companies and private-held firms. PLC boards tend to be 'low touch' with a monitoring and compliance emphasis, whereas PHF boards tend to be 'high tough' and the focus is on strategy and business performance.

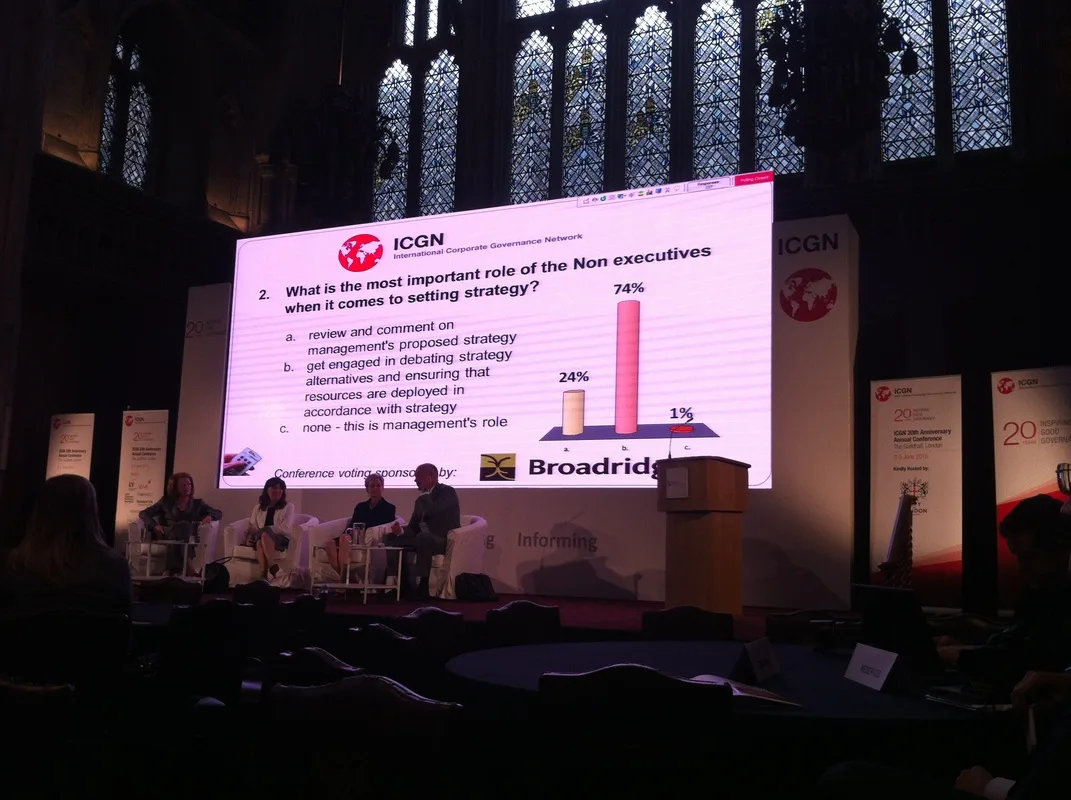

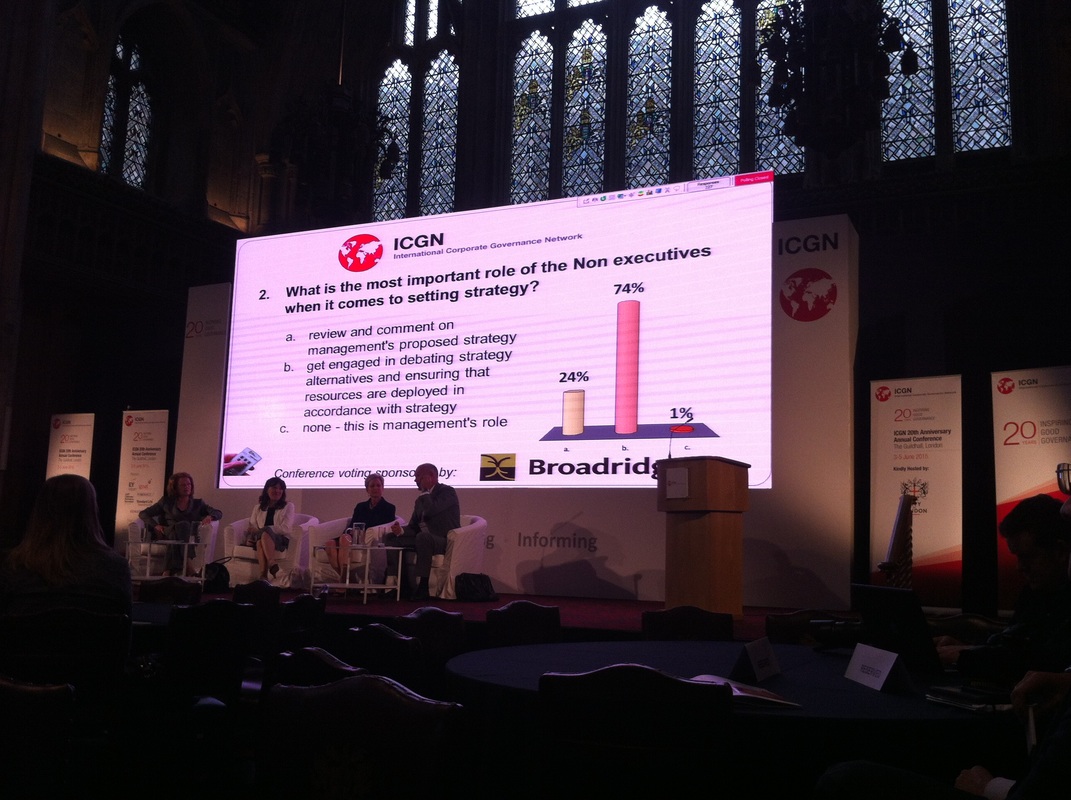

- Boards need to get far more involved with the consideration of strategic options than most do now (cf. my research, which suggests that an active involvement in strategy development is crucial).

- Most shareholders and institutional investors 'know' that boards need to be involved in strategy development (per the survey result below), yet precious few boards actually take the task of strategy development and strategy management as seriously as the survey suggests is required.

- Directors need to be fully informed on all material matters. Suggested channels included formal due diligence; asking probing questions of rhe chair executive during board meetings; eliciting information from multiple sources; asking for information to be presented in a particular format.

- Boards need to be high-trust environments, whereby directors are free to debate the issues (heatedly sometimes) in the pursuit of an agreed company purpose and strategy.

- One panel member took the position that expecting that 'board involvement in 'strategy' might be expecting too much from directors (even though directors have a duty of care to make enquiries and become adequately informed.

These takeaways demonstrate that boards are starting to thinking about future business performance. However, there is much work to do, both by boards to determine an appropriate division of labour between the board and management, and by shareholders to express their wishes more clearly than perhaps now is the case.