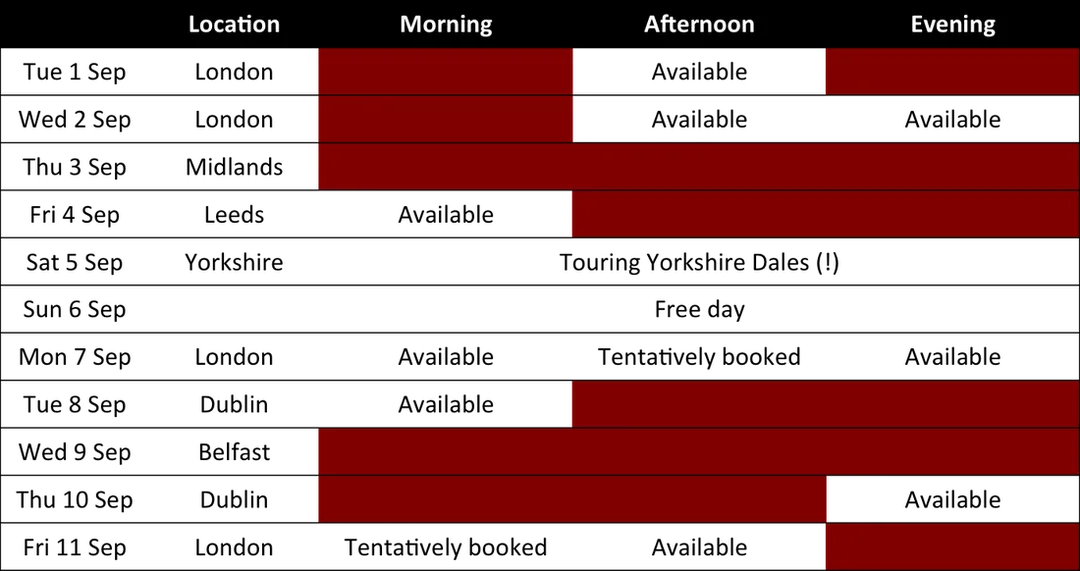

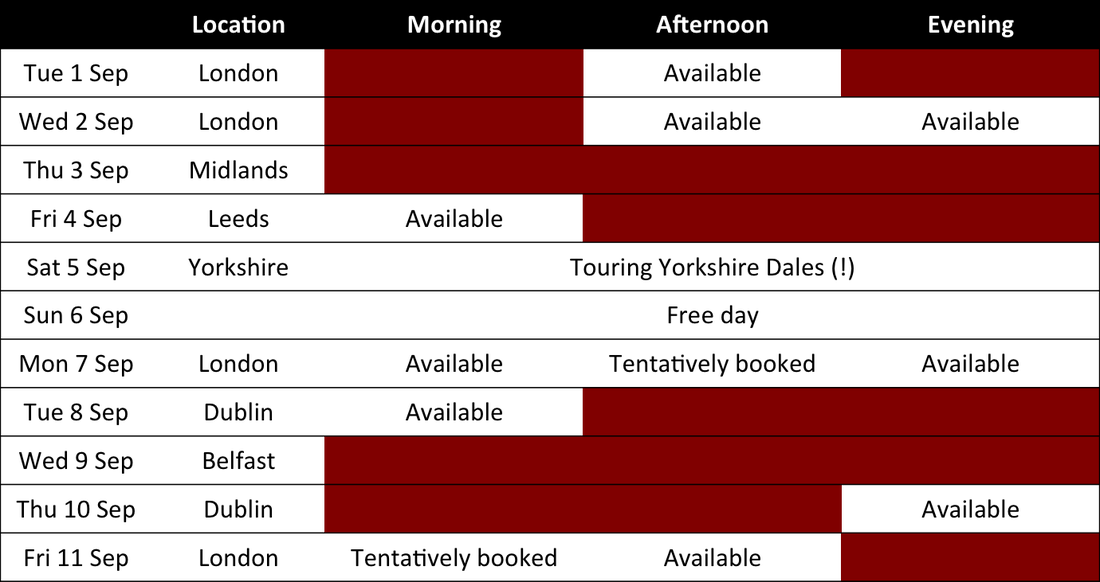

Plans for my next trip to Great Britain and Ireland—a speaking and advisory tour to share insights from my latest research and practical experience in boardrooms—are starting to come together. My schedule is filling up—only a third of the available slots are still available. Thank you to everyone who has already reserved space. The dates and times you have requested are secure.

If you are based in London (or the home counties), Leeds (or elsewhere in Yorkshire) or Dublin; and you want me to address your board or executive team, discuss a future speaking or advisory engagement, or chat privately about a difficult challenge, please get in touch soon to avoid disappointment. I look forward to hearing from you, and then to discussing any aspect of board practice, corporate governance, strategic management, value creation or business performance that is of interest to you.