|

The topic of gender diversity on boards has received a lot attention in recent years. Researchers, interest groups and the media have chased various agendas. Much has been written and many claims have been made. However, compelling conclusions remain elusive. The topic received more attention during the first session of the second day of the International Governance Workshop in Barcelona. Three speakers presented the results of their research, conducted in the Polish and Spanish contexts. The studies explored variations on the theme of the impact of women on various financial and non-financial measures. All of the studies were quantitative analyses, conducted using publicly available data and statistical techniques. I have been critical of the use of such techniques for social research in the past. Reductivist approaches rarely provide insight beyond straightforward correlations. Sadly, I heard nothing to suggest otherwise in these talks. The challenge for board research is to move beyond the 'big three' assumptions--ontological reductionism, that a single objective reality might exist, and that a constant conjunction between variables constitutes a causal explanation—are inapplicable to board research, because boards and the context within which they exist, companies, are social constructions. Rather, the more demanding route, of qualitative research that explores boards in situ is more likely to reveal explanations that shareholders and director nomination committees can rely on. I remain convinced that women and people from a diverse range of background affect board practice. However, simple empirical research is not the appropriate pathway to understand and explain whether this is correct is not. More subtle approaches, that consider the context and behavioural nuances of individual directors appears to be crucial.

0 Comments

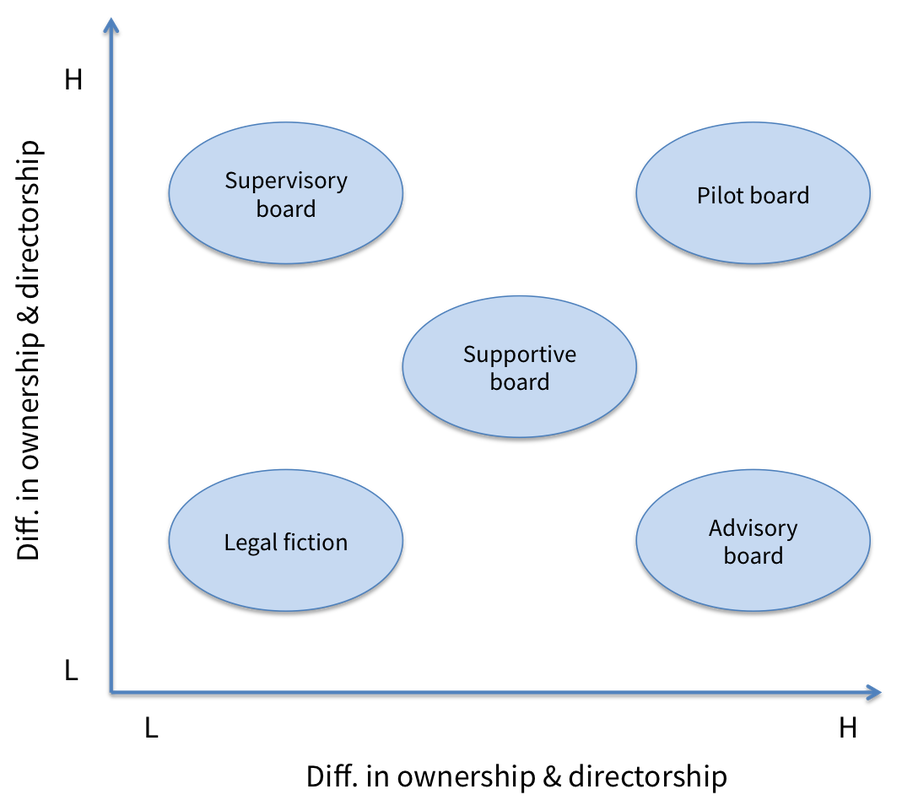

A team of researchers from Spain, France and New Zealand have been collaborating on an interesting project: one of understanding how board roles and contributions change in different firm circumstances. Khlif, Karoui and Ingley have identified five 'roles' that appear to emerge as firm circumstances change in two dimensions, as follows:  The difference in the way the boards work (in terms of performing control, service, strategy and mediating tasks) appears to vary quite markedly when the difference between ownership and directorship is high (the directors are not owners), and when the difference between ownership and management is high (the managers and directors are not the same people). The paper offered some interesting insights relating to the emergence of corporate governance as a system within SMEs, and highlighted the need for a holistic, integrated consideration of board roles and board research, one that takes the company objectives and configuration into account. The research, to understand what this insight might actually mean is continuing apace.

The second International Governance Workshop got underway at Toulouse Business School, Barcelona Campus on Thursday 11 June 2015. Professor Morten Huse, an esteemed corporate governance scholar from Norway, provided the opening day keynote. Huse has been studying boards for a long time—the mid 1970s—so when he speaks, people tend to listen. Here's four of the points from his talk: Huse's talk set the scene for a lively debate through the balance of the conference. It will be very interesting to see how this develops.

The annual International Governance Workshop, hosted by the Toulouse Business School, starts tomorrow in Barcelona. Although only in its second year, this conference is an important gathering because it has attracted many of the world's leading corporate governance and board researchers. To be in the same room as these people, to hear them present and debate the results of emergent research is truly an honour. In contrast to the scale of the ICGN annual conference, the IGW is more intimate and more focussed. However, the programme of topics to be explored is no less significant. Session summaries will be posted here, as usual, so you can keep up to date. My paper will be delivered on Thursday afternoon.

Martin Wolf CBE, Associate Editor and Chief Economics Commentator at the Financial Times, delivered a rousing keynote talk to wrap up the final day of the ICGN annual conference. After observing that the limited liability, joint-owned corporation had been the cause and consequence of almost all economic activity over the last two hundred years, Wolf posed and commented on four questions. He qualified his comments by saying that he expected they might raise some profound questions. Indeed, some of Wolf's comments were controversial—the evidence being the questions asked by some members of the audience after he finished speaking. What is a limited liability corporation? They are a semi-permanent entity designed to outlast small-medium enterprises (because founders retire—the corner store conundrum) and markets, and they are a construct for the consolidation of relational and implicit contracts. Their genius is the importation of older hierarchical forms (to get things done) into the market system. With scale comes efficiency, endurance and effectiveness (but not always!). What is their purpose? The apparent purpose of the LLC is to generate economic value. However, this is insufficient. Wolf asserted that LLCs should also pursue a wider remit, by seeking to 'add value' in social terms (through the provision of payments for services rendered—wages and salaries—for example). What is their operational goal? The oft-quoted goal, of maximising shareholder returns, is far too simplistic, according to Wolf. It is selfish and can only lead to failure elsewhere in society. Rather, the operational goal of LLCs needs to include ethical constraints to protect all participants and in so doing ensure the good of society (at no point did Wolf pursue or even imply any form of Marxist agenda). Who should control them? Economically, shareholders bear residual risks following corporate activity and, therefore, shareholders should possess control rights. Wolf challenged this commonly-held view as folly because shareholders are unable to exert full control over the affairs of the corporation. Managers may manipulate the affairs of the company, sometimes to the detriment of shareholders and other stakeholders. Short-term incentives, implemented to motivate managers towards the maximisation of shareholder returns, rarely position the company for longer-term success. Wolf concluded by saying that LLCs are a wonderful construct. However, he went on to say that the two associated doctrines (of shareholder control and value maximisation) are unhelpful because they are too short-sighted. He told the shareholders in the room that "it is in your interest not to control the corporation completely". Other parties—large bondholders, for example—also bear residual risks. Why would they not have decision rights? Wolf's comments were demonstrably controversial (amongst some of the audience at least). However, the poor reputation of big business amongst the general populace suggest Wolf's comments might be closer to the 'truth' than what many in the audience might care to admit. Wolf closed with this demanding challenge: A better approach might be "to let a hundred flowers bloom", so that the best [control] model might rise up and be applied for a given situation—the beneficiary being society at large.

Robert AG (Bob) Monks is a experienced shareholder activist and pioneer in corporate governance. The tall octogenarian has spent a lifetime influencing boards and board performance, especially in corporate America. Monks was invited to deliver the keynote address the ICGN conference. Monks, a gifted orator, spoke from the heart, and he had the gathered delegates enthralled as he did so. Reviving memories of the wartime leader Winston Churchill, Monks reminded delegates that, while they had come far, they were not at the end (ie. 'arrived') nor were they at the beginning of the end. They were, he said, "at the end of the beginning". He went on to suggest:

Monks continued by offering several recommendations to the audience (comprised largely of institutional investor representatives but also other participants in the corporate governance community including academics and advisors). He said that shareholders need to be genuinely engaged (by specifying what they want from their investment); that integrated reporting is crucial (to provide clarity around actual business performance); and, that all publicly-listed companies need to have real (identifiable) owners (to satisfy the engagement challenge. Monks received a standing ovation from some of the delegates, such was the power of his oratory and the high esteem in which he is held. One surprise: neither value creation or strategy was mentioned. I wonder what Monks thinks about these activities and the board's role therein. Rather than guess, I'm going to ask him. Congratulations to the conference organisers for securing Bob Monks' contribution to the debate.

The 15th European Academy of Management (EURAM) annual conference will be held in Warsaw, Poland on 17–20 June. The conference programme is now available online. Over 1200 delegates have registered to attend, to hear about the latest developments in management research and the implications for practice. I am looking forward to attending what promises to be a very interesting (and busy!) conference. EURAM is the third of three international conferences that I will be attending in June. In addition to listening to as many of the corporate governance papers as possible and meeting with colleagues, I have two formal commitments, as follows:

If you would like to receive more information about any of the papers, please let me know. I will do my best to attend the appropriate session and write a report.

Please excuse this rather sensationalist title—I have just picked myself up from the floor having read this clause in the recital section of a [draft] directive being prepared in the EU: "Although they do not own corporations, which are separate legal entities beyond their full control, shareholders play a relevant role in the governance of those corporations." The proposed directive, which encourages long-term engagement and gives voice to shareholders in listed companies and large companies, seems to be well intentioned. However, the statement that shareholders do not own the corporation left me flabbergasted. It raises all sorts of questions:

Why anyone would buy an asset if they knew that a condition of purchase was that they did not own what they had just paid for is beyond me. Is this sloppy drafting, or have I missed something in the semantics? Can someone with a legal mind and expertise in this area please elucidate?

Most people I know live fairly busy lives. Western culture and the 'always on' society we live in has done that to us. However, some—by my assessment anyway—have become a bit too busy for their own good. Societal norms seem to reward busyness and excellence, yet cracks start to appear when we get very busy for long periods. We get tired and make mistakes. Our commitment to do things with excellence suffers. How do you cope in such situations? Do you plan well ahead; or, do you manage your commitments on a daily basis; or, do you simply back yourself to keep up with what work and life serves up? One habit that has served me well for many years is the 'heads-up' habit. It's really simple. Every week, I pause and look ahead, as follows:

In the past, I sometimes lost sight of important upcoming activities (and ended up suffering late into the night trying to make up—the results of which were never that great). However, last-minute rushes have become a rarity since I embraced the heads-up habit. If you don't have a habit to stay of top of your commitments, you might like to try this one. It made my life easier and I seem to be more productive. Also, my wife says that I'm easier to live with!

We live in a paradoxical world. Rates of change are increasing, yet we want certainty. Times to market are reducing, yet we still want instant gratification. Zafer Achi and Jennifer Garvey Berger explored these paradoxes recently. They acknowledged that searches for certainty are "only natural", and that managers spend much of their time "managing the probable". However, the world is a social place. People make choices and things change, often unexpectedly. Consequently, the best laid plans can fail completely, leaving managers exposed and potentially out of a job. Achi and Berger suggest that the frame of reference used by most managers, of managing the probable, is a big part of the problem. Rather than managing the probable, they suggest that managers need to "lead the possible". They offered three recommendations to help managers make the change (see article for details):

These recommendations have the potential to change the way managers think, make decisions and lead. While reading the article, I couldn't help but think that the recommendations also have application in the boardroom. However, the adoption of 'possibility' thinking would up-end board practices in many cases. Boards that spend most of their time monitoring past performance and controlling the activities of the chief executive would probably be quite uncomfortable, even though the recommendations are neither earth-shattering nor inconsistent with the role and responsibility of the board (to maximise performance in accordance with the wishes of shareholders). Maybe its time for directors to take stock.

|

SearchMusingsThoughts on corporate governance, strategy and boardcraft; our place in the world; and other topics that catch my attention.

Categories

All

Archives

April 2024

|

|

Dr. Peter Crow, CMInstD

|

© Copyright 2001-2024 | Terms of use & privacy

|